When your mutual fund shows a 12% annual return, it feels like you’ve made it, right? The numbers look great on paper, your SIP is growing, and everything seems to be going just fine.

But here’s a truth bomb:

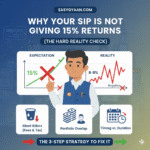

Even after earning 12% per annum, you might still be losing money.

Sounds shocking? Let’s break it down.

The Illusion of “Good Returns”

Suppose you invested ₹6 lakhs over time — through a SIP or lump sum. After 5 years, your investment grows to around ₹10.52 lakhs, assuming a consistent 12% CAGR (Compound Annual Growth Rate).

At first glance, this seems like solid growth — a gain of over ₹4.5 lakhs. People often take this number and start feeling financially confident. Some even start planning holidays or upgrades.

But here’s what they miss: This figure is not your real earning.

Tax and Inflation — The Hidden Killers

We often forget that what we see is not always what we get.

Let’s now subtract two invisible forces that quietly eat into your wealth:

- Capital Gains Tax

- Inflation

1. Long-Term Capital Gains (LTCG) Tax (As of 2025)

From July 2024, the Government of India revised the LTCG tax on equity mutual funds:

- 12.5% LTCG on gains exceeding ₹1.25 lakh per year

- No indexation benefit

2. Inflation: The Silent Eroder

Inflation in India averages around 6% per year. That means what costs ₹100 today will cost ₹134 in 5 years. So, unless your money grows faster than inflation, your purchasing power actually falls.

Let’s Crunch the Numbers

| Particulars | Amount (₹) |

|---|---|

| Investment | ₹6,00,000 |

| Value after 5 years @12% CAGR | ₹10,52,000 |

| Capital Gain | ₹4,52,000 |

| LTCG Exemption (as per new rule) | ₹1,25,000 |

| Taxable Gain | ₹3,27,000 |

| LTCG Tax @12.5% | ₹40,875 |

| Post-Tax Value | ₹10,11,125 |

| Value after adjusting for 6% inflation | ~₹7,50,000 (approx.) |

| Real Gain | ~₹1.5 lakh over 5 years |

| Effective Real Return (CAGR) | ~5.2% |

So, while your investment showed a 12% return, your actual real return is just around 5%.

And this is before considering fund fees or exit loads!

What Most Investors Overlook

The mutual fund industry often showcases CAGR in bold. But CAGR is a nominal number — it doesn’t account for real-life factors like tax or inflation.

Most retail investors:

- Don’t factor in LTCG

- Don’t adjust for inflation

- Celebrate the “growth” without understanding the actual value added

This isn’t just a math problem. It’s a mindset gap.

Why Real Return Matters

Let’s say your money grows at 12% but inflation is 6%, and LTCG takes another 1.5% yearly on average.

Your effective wealth growth is barely 4.5% — and that’s not enough if you’re aiming for major goals like retirement, children’s education, or buying a home.

Remember:

“It’s not about how much you earn, but how much you keep — and what it can buy in the future.”

Smart Investors Think Differently

To really grow wealth, you must look beyond headline returns. Here’s how savvy investors do it:

1. Use Tax-Efficient Investment Vehicles

- Index Funds: Less portfolio churn = lower realized capital gains

- ELSS (Equity Linked Saving Scheme): Comes with ₹1.5 lakh deduction under Section 80C + LTCG applies only on actual withdrawals

- Long-Term Holding: Avoid frequent buying/selling which triggers capital gains

2. Always Adjust for Inflation

When setting financial goals, don’t just say “I need ₹50 lakhs in 10 years.” Ask:

- “What will ₹50 lakhs be worth in 10 years after 6% inflation?”

- Use real return calculators to plan better

3. Look at Real CAGR

Before celebrating a 12% return, ask:

- What’s the post-tax return?

- What’s the post-inflation return?

- Is it aligned with my financial goal timeline?

The Mindset Shift You Need

Most people are emotionally driven investors. If their fund shows a ₹3 lakh profit, they think they’re rich.

But real investors think long-term:

- They focus on wealth preservation and growth

- They evaluate investments based on net gain in purchasing power

- They’re realistic about taxes, fees, and market risks

Real investing is not about feeling good — it’s about doing the math.

Key Takeaways

- A 12% CAGR doesn’t mean a 12% profit in real life.

- After the new 12.5% LTCG rule and 6% inflation, your real return may drop to ~5%.

- Always calculate post-tax, post-inflation returns before judging performance.

- Use tax-efficient strategies and review your portfolio with real growth in mind.

Final Thoughts

So, the next time someone says, “My SIP gave me 12% returns,” smile politely — and ask,

“Is that before or after tax and inflation?”

Because true financial literacy begins when you stop chasing shiny numbers and start understanding value.

For more no-fluff, honest financial content, follow Easy Finance on YouTube and visit easygyaan.com — where we simplify money, investing, and everything in between.

Leave a Reply