Confused between SIP and Lumpsum? This 2025 guide breaks down both strategies using real 15-year data from HDFC Mid-Cap Fund. Learn when to use SIP, when Lumpsum works better, and how to combine both for smart investing.

Introduction: It’s Not a Contest, It’s a Journey

In 2025, most Indian investors still find themselves asking: “SIP or Lumpsum — which one is better?”

But here’s the truth no one tells you: SIP and Lumpsum are not rivals. They’re tools for different stages of your wealth journey.

- SIP (Systematic Investment Plan) is ideal when you’re starting from zero, helping you accumulate wealth slowly and steadily.

- Lumpsum is powerful after you’ve built a corpus — it accelerates your growth when used strategically.

Instead of thinking “either-or”, the right question is: What phase of your life are you in — accumulation or expansion? This blog post will show you how to decide, using real-world data and a clear framework you can act on immediately.

SIP vs Lumpsum: What Do They Really Do?

Let’s skip the beginner-level definitions. You already know SIP means investing regularly and Lumpsum means investing a large amount at once.

What matters is how they behave over time, especially in the unpredictable Indian market.

- SIP: Reduces the impact of market volatility. Helps inculcate saving discipline. Ideal for salaried or monthly earners.

- Lumpsum: Makes the most of market dips. Works when you have idle cash. Ideal for deploying bonuses, sale proceeds, or inherited funds.

But don’t just take theory — let’s dive into actual results.

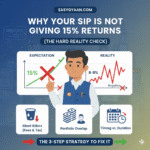

Real-Life Data: SIP vs Lumpsum in HDFC Mid‑Cap Opportunities Fund

We took one of India’s best-performing mutual funds — HDFC Mid‑Cap Opportunities Fund – Growth Plan — and looked at a 15-year performance window from August 2010 to July 2025.

SIP Investment

- ₹5,000/month invested from Aug 2010 to July 2025

- Total investment: ₹9,00,000

- Final corpus: ~₹49,00,000

- XIRR (Effective CAGR): ~20.55%

Lumpsum Investment

- ₹1,00,000 invested in Aug 2010

- Final corpus: ~₹13,00,000

- CAGR: ~18.96%

Side-by-Side Comparison:

| Strategy | Total Invested | Final Corpus | CAGR/XIRR |

|---|---|---|---|

| SIP | ₹9,00,000 | ₹49,00,000 | ~20.55% |

| Lumpsum | ₹1,00,000 | ₹13,00,000 | ~18.96% |

SIP delivered higher total returns and a better CAGR, even though the investment was gradual.

Lumpsum delivered strong growth too, but it required upfront capital and emotional discipline during volatile years.

This clearly shows that SIP is not a compromise — it’s a strategy that builds wealth reliably over time.

Why SIP and Lumpsum Are Not Comparable

Too many investors try to compare SIP and Lumpsum returns side by side — that’s flawed.

Here’s why:

- SIP is for people starting from scratch — helping them build their investment muscle gradually.

- Lumpsum is for those who already have money saved up and are ready to grow it quickly.

Think of SIP as building bricks over time. Think of Lumpsum as putting a rocket on top of what you’ve already built.

So, it’s not about choosing one over the other. It’s about using each at the right time.

When to Use SIP

- You earn a regular monthly salary

- You’re new to mutual fund investing

- You want to avoid timing the market

- You prefer consistent, automated investing

- You are building a retirement or long-term education fund

SIP is also psychologically easier — you invest small amounts, don’t worry about timing, and build wealth silently.

When to Use Lumpsum

- You receive a large bonus or inheritance

- You sold property or an FD just matured

- You see a market correction and want to take advantage

- You’re investing with a 10+ year horizon

But here’s the catch: investing a large amount at once can feel risky. That’s why many investors prefer a hybrid strategy.

Smart Strategy: Combine SIP + Lumpsum

The best investors don’t pick sides — they use both.

Example:

- Continue ₹5,000 SIP every month

- Invest ₹2 lakh bonus through STP (Systematic Transfer Plan) over 6 months

- This allows you to average your lumpsum and reduce timing risk

You get the benefit of discipline (SIP) and opportunity (Lumpsum/STP) without emotional stress.

Taxation: Same for Both, But Be Smart

In 2025, LTCG (Long-Term Capital Gains) tax on equity funds works as follows:

- Tax-free up to ₹1.25 lakh/year

- 12.5% tax on gains exceeding that limit

💡 SIP investors need to remember that each installment has its own holding period. Plan withdrawals carefully.

Common Mistakes to Avoid

- Waiting too long for the “perfect market” to invest a lumpsum

- Stopping SIPs during market crashes (that’s when they help most)

- Investing without a goal or timeline

- Ignoring asset allocation (debt, equity, gold)

- Thinking SIP is “low return” — real data says otherwise!

Final Thought: Accumulate First, Grow Next

Let’s bring it all together:

| Phase | Ideal Strategy |

|---|---|

| Starting your journey | SIP |

| After corpus is built | Lumpsum or STP |

| Want to invest bonus | Lumpsum (if confident) or STP |

| Market is volatile | Continue SIPs |

SIP helps you accumulate the foundation. Lumpsum helps you scale up faster once you’re ready.

The smartest strategy? Do both. Let SIP run in the background. Use Lumpsum when opportunity strikes.

Conclusion

In 2025, with mutual fund access easier than ever, the real challenge is not picking SIP vs Lumpsum — it’s understanding how to use both wisely.

Don’t think in terms of returns alone. Think in terms of:

- When you’re investing

- Why you’re investing

- And how much you can commit emotionally

Because wealth isn’t built in one shot. It’s built with clarity, consistency, and confidence — one SIP and one Lumpsum at a time.

References

- Data sourced from user-verified calculations and mutual fund tools like StarSIP, Groww, and Moneycontrol.

Disclaimer:

This blog post is for informational purposes only and reflects independent analysis. Mutual fund investments are subject to market risks. Please consult a SEBI-registered financial advisor before making any investment decisions.

Some useful links – How to Plan Your Retirement

Leave a Reply