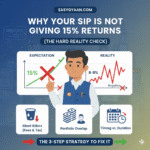

Discover the top 5 common SIP mistakes Indian investors make and learn how to fix them. Maximize your mutual fund returns with these expert tips.

In the last few years, the Systematic Investment Plan (SIP) has become a household name in India. From tea-stall discussions to corporate boardrooms, everyone is talking about “SIP karna hai.” According to AMFI data, the monthly SIP contribution in India has consistently crossed the ₹20,000 crore mark, proving that the retail investor has finally embraced the power of equity.

However, simply starting an SIP isn’t a guarantee of wealth. Many investors “set it and forget it” in the wrong way, leading to mediocre returns or, worse, capital loss. If you feel your portfolio isn’t growing as it should, you might be making one of these five common mistakes.

1. Stopping SIPs During Market Downturns (The “Panic” Mistake)

This is the single most destructive mistake an Indian investor can make. When the Nifty 50 drops by 10% or 20%, the natural human instinct is to protect what is left. Investors often stop their SIPs, thinking, “I will restart when the market stabilizes.”

Why it’s a mistake:

SIPs work on the principle of Rupee Cost Averaging. When the market falls, your fixed SIP amount buys more units of the mutual fund. When the market eventually recovers, these extra units purchased at “discounted” prices are what drive your exponential growth.

The Fix:

Treat market crashes as a “Flash Sale.” If you were happy buying units at a NAV of ₹100, you should be ecstatic buying them at ₹80. Unless you have a genuine financial emergency, never stop your SIP during a bear market.

2. Choosing “Regular” Plans Instead of “Direct” Plans

Many investors still start SIPs through their local bank branch or an agent. These are usually Regular Plans. While they seem convenient, they come with a hidden cost: Commissions.

Why it’s a mistake:

In a Regular Plan, the mutual fund company pays a commission (usually 0.5% to 1.5% per year) to the agent from your money. This is reflected in a higher Expense Ratio. While 1% sounds small, over 20 years, it can eat away up to 20-25% of your final wealth due to the lost opportunity of compounding on that commission.

The Fix:

Switch to Direct Plans. You can do this through the AMC’s website or reputable platforms that offer direct mutual funds. The underlying portfolio is the same, but the lower expense ratio means more money stays in your pocket.

3. Having No “Step-Up” Strategy

Most investors start an SIP of, say, ₹5,000 and keep it the same for five or ten years. While this is better than not investing, it fails to account for inflation and your rising income.

Why it’s a mistake:

As your salary increases, your lifestyle usually expands (lifestyle inflation). If your investment remains stagnant, your future corpus will not be enough to maintain your standard of living after retirement.

The Power of a 10% Step-Up:

- Scenario A: ₹10,000 monthly SIP for 20 years at 12% = ~₹1 Crore.

- Scenario B: ₹10,000 monthly SIP with a 10% annual increase for 20 years at 12% = ~₹2.2 Crores.

By simply increasing your SIP by a small amount every year, you can more than double your final corpus.

4. Investing Without a Specific Goal (The “Vague” Approach)

“I want to create wealth” is a wish, not a goal. Many Indians start SIPs without knowing when they will need the money or what it is for.

Why it’s a mistake:

Without a goal, you won’t know:

- Which fund to pick: You shouldn’t put money for a 2-year goal (like a car) into a Small-cap fund.

- When to exit: If you don’t have a target, you might stay in equity for too long and lose your gains in a last-minute market crash right before you need the money.

The Fix:

Tag every SIP to a goal.

- SIP A: Retirement (Equity Diversified/Index) – 20 years.

- SIP B: Child’s Education (Midcap/Aggressive Hybrid) – 12 years.

- SIP C: Home Downpayment (Debt/Conservative Hybrid) – 3 years.

5. Chasing Last Year’s Top Performers

This is the “Rear-View Mirror” syndrome. Investors often look at the “Top 5 Funds of 2024” and move all their money there in 2025.

Why it’s a mistake:

Mutual fund categories move in cycles. The best-performing fund of last year is often the one that took the highest risk or was in a sector that is now overvalued. By the time you invest, the “rally” might already be over. This leads to a cycle of buying high and selling low.

The Fix:

Focus on Consistency rather than “Star Ratings.” Look for funds that have consistently beaten their benchmark over 5 and 10-year periods, even if they aren’t the #1 performer in a single year.

Summary Table: SIP Mistakes vs. Smart Moves

| Common Mistake | The Smart Move | Impact on Wealth |

| Stopping SIP in a crash | Continue (or increase) SIP | High (Averaging benefit) |

| Investing in Regular Plans | Switch to Direct Plans | Very High (Saves 1% annually) |

| Fixed SIP amount | Annual Step-up (Top-up) | Massive (Beats inflation) |

| Investing without goals | Goal-based tagging | High (Right Asset Allocation) |

| Chasing recent winners | Choose consistent performers | Moderate (Reduces volatility) |

Conclusion: The Secret is Discipline

The beauty of a Systematic Investment Plan is that it is designed to work for common people who don’t have time to track the stock market every hour. The “Systematic” part is more important than the “Investment” part.

If you avoid these five pitfalls—staying invested during dips, choosing direct plans, stepping up your contributions, defining your goals, and ignoring short-term hype—you are already ahead of 90% of retail investors in India.

Leave a Reply