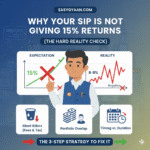

“Why is your SIP return low? Explore the hard reality of mutual fund investing in India. Avoid common mistakes and learn the Step-Up strategy for wealth growth.”

Every Indian investor has done it. You open an online SIP calculator, enter ₹5,000, set the expected return to 15%, and slide the tenure to 20 years. The screen flashes a massive corpus of nearly ₹75 Lakhs. It looks easy, predictable, and incredibly exciting.

But then reality hits.

You’ve been investing for three years, and when you finally check your portfolio, the returns aren’t 15%. They are 8%, or 9%, or in some bad months, even negative. Naturally, the doubts creep in: Is my fund manager incompetent? Is the market rigged? Is the “SIP magic” just a marketing gimmick?

I am Abhijit Khare, and today at Easy Gyaan, we are going to do a reality check. We will uncover the three “Secret Reasons” why your SIP isn’t hitting that dream 15% mark and, more importantly, how you can fix it.

The Illusion of the “Smooth Line”

The biggest problem is that SIP calculators show a smooth, upward-curving line. In the real world, the market moves like a rollercoaster. To reach a long-term average of 15%, the market has to go through years of -10% and years of +40%.

If you are currently seeing low returns, you aren’t necessarily failing; you might just be in the “boring” or “painful” phase of the cycle. Let’s dive into the technical reasons why your numbers aren’t matching the calculator.

1. The “Timing vs. Duration” Gap (Sequence of Returns)

In theory, SIP is meant to eliminate the need for timing the market. While this is true for long-term wealth, the time you start heavily impacts your “Point-to-Point” returns in the short run.

The Tale of Two Investors

Imagine two friends, Rahul and Anjali.

- Rahul started his SIP in 2021 during the post-pandemic bull run when markets were at an all-time high.

- Anjali started her SIP in 2023 when the market was undergoing a correction and felt “flat.”

If both check their portfolios today, Anjali will likely show a much higher XIRR (returns) than Rahul. Why? Because Rahul bought his early units at high prices, while Anjali bought her early units at a discount.

The Patience Test

If the Nifty 50 grows by only 5% in a year, no fund manager can magically give you 15%. A 15% CAGR is an average, not a guarantee. To get that 15%, you must have the patience to sit through the years when the market does nothing, so you are present when the market eventually jumps 40% in a single year.

2. The Silent Killers: Understanding Net Returns vs. Gross Returns

When you see a “15% Return” on a website, that is the Gross Return of the fund’s assets. What actually lands in your bank account is the Net Return, and there are three “silent killers” that eat into your wealth.

A. The Expense Ratio (The Leaking Bucket)

Every mutual fund charges a fee to manage your money, known as the Expense Ratio. If your fund earns 15% but has an expense ratio of 2%, your actual return is 13%. Over 20 years, that 2% difference can reduce your final wealth by lakhs of rupees.

- Pro Tip: Always opt for Direct Plans over Regular Plans to save on distributor commissions.

B. Exit Loads and Shifting Costs

If you panic and withdraw your money within a year, most equity funds charge an “Exit Load” of around 1%. This immediately reduces your performance. Frequent “fund hopping” (switching funds based on last year’s performance) is a sure-fire way to kill your compounding.

C. The New Tax Regime (LTCG)

As per the latest Indian tax laws, Long Term Capital Gains (LTCG) above ₹1.25 Lakh in a financial year are taxed at 12.5%. When you use a calculator, you are looking at pre-tax wealth. In reality, after paying the fund management fees and the government’s tax, your “15% dream” often translates to an 11-12% reality in hand.

3. Portfolio Overlap: The “Di-worsification” Trap

Most Indian investors hold too many funds. I’ve seen portfolios with 10 or 15 different mutual funds. The investor thinks they are being safe by diversifying, but they are actually doing “Di-worsification.”

The Hidden Mirror

If you own five different ‘Large Cap’ funds, chances are 80% of their holdings are the same stocks: Reliance, HDFC Bank, ICICI Bank, and Infosys. By holding so many similar funds, you have accidentally created an expensive Index Fund. You are paying high fees for “Active Management,” but your returns will only match the Market Index (which might be 12%) because you own the whole market anyway.

This “Average Joe” portfolio will never generate the “Alpha” (excess return) needed to hit 15-18%.

How to Actually Achieve 15% Returns: The 3-Step Strategy

Knowing the problems is half the battle. Here is the strategy to actually boost your portfolio performance.

Step 1: The Step-Up SIP (Your Secret Weapon)

Don’t keep your SIP amount stagnant. As your salary increases, your investment must increase. By adding a 10% annual Step-Up to your SIP, you can reach your goals much faster, even if the market returns are slightly lower than 15%. This compensates for inflation and tax leakages.

Step 2: Lumpsum “Top-ups” on Dips

Smart investors don’t just rely on the automated SIP. When the market crashes by 3-5% in a single week, or when the Nifty touches its 200-Day Moving Average, put in a small Lumpsum amount. This lowers your average purchase cost significantly and acts as a “turbo-charger” for your returns.

Step 3: Portfolio Clean-up (The “Core 4” Rule)

Stop collecting mutual funds like postage stamps. A clean, high-performance portfolio usually only needs 4 types of funds:

- Flexi Cap Fund: For Go-anywhere flexibility.

- Large Cap / Index Fund: For stability.

- Mid Cap Fund: For growth.

- Small Cap Fund: For high-risk, high-reward “Alpha.”

Review your portfolio every six months. If a fund is consistently underperforming its benchmark for more than two years, it’s time to say goodbye.

Conclusion: Discipline Over Magic

15% is not a magic number; it is the reward for discipline. If your portfolio is looking red or flat right now, don’t panic. Review your strategy, check your expense ratios, and ensure you aren’t over-diversified.

Wealth creation via SIP is a marathon, not a sprint. If you stay the course and use the “Top-up” strategy during market dips, the math will eventually work in your favor.

Are you unsure if your current Mutual Fund portfolio is built correctly? At Easy Finance, we help you cut through the noise. If you want a professional review of your portfolio to ensure you are on track for your goals, feel free to reach out to us via WhatsApp or Call at +91 8010924901.

Some Useful Links – Top 5 Mistakes Indian Investors Make with SIPs (And How to Fix Them)

Author Bio: Abhijit Khare

Abhijit Khare is a seasoned Business Development Consultant and the founder of Easy Finance. With a deep passion for the Indian markets, he specializes in simplifying complex financial concepts like Mutual Funds, SIP strategies, and Nifty trading. Through his YouTube channel and blog, Abhijit is on a mission to help retail investors move beyond “average” returns and build a high-alpha portfolio for long-term wealth.

Leave a Reply